How Health Savings Accounts (HSAs) Work in the U.S.

A Health Savings Account (HSA) is a tax-advantaged savings account designed to help individuals in the United States save and pay for qualified medical expenses. These accounts are available to people enrolled in high-deductible health plans (HDHPs) and offer several financial benefits, including tax savings, long-term growth, and flexibility.

What is an HSA?

An HSA allows you to set aside pre-tax money to cover medical costs such as doctor visits, prescriptions, vision care, dental treatments, and even some over-the-counter items. To open an HSA, you must be enrolled in an HSA-eligible high-deductible health plan.

HSAs are owned by the individual—not the employer—and the money in the account rolls over from year to year. This means you won’t lose unused funds at the end of the year, making HSAs a useful tool for both short-term medical spending and long-term health savings.

Key Benefits

-

Triple Tax Advantage

-

Contributions are tax-deductible

-

Earnings grow tax-free

-

Withdrawals for qualified health expenses are also tax-free

-

-

Rollover and Portability

Funds in an HSA never expire. The account stays with you even if you change jobs or retire. -

Investment Options

Many HSA providers allow you to invest funds once you reach a certain balance, helping your money grow over time.

2025 Contribution Limits

According to IRS guidelines:

-

Individual coverage: $4,150 per year

-

Family coverage: $8,300 per year

-

Catch-up contribution (age 55+): Additional $1,000

These limits are adjusted annually to account for inflation.

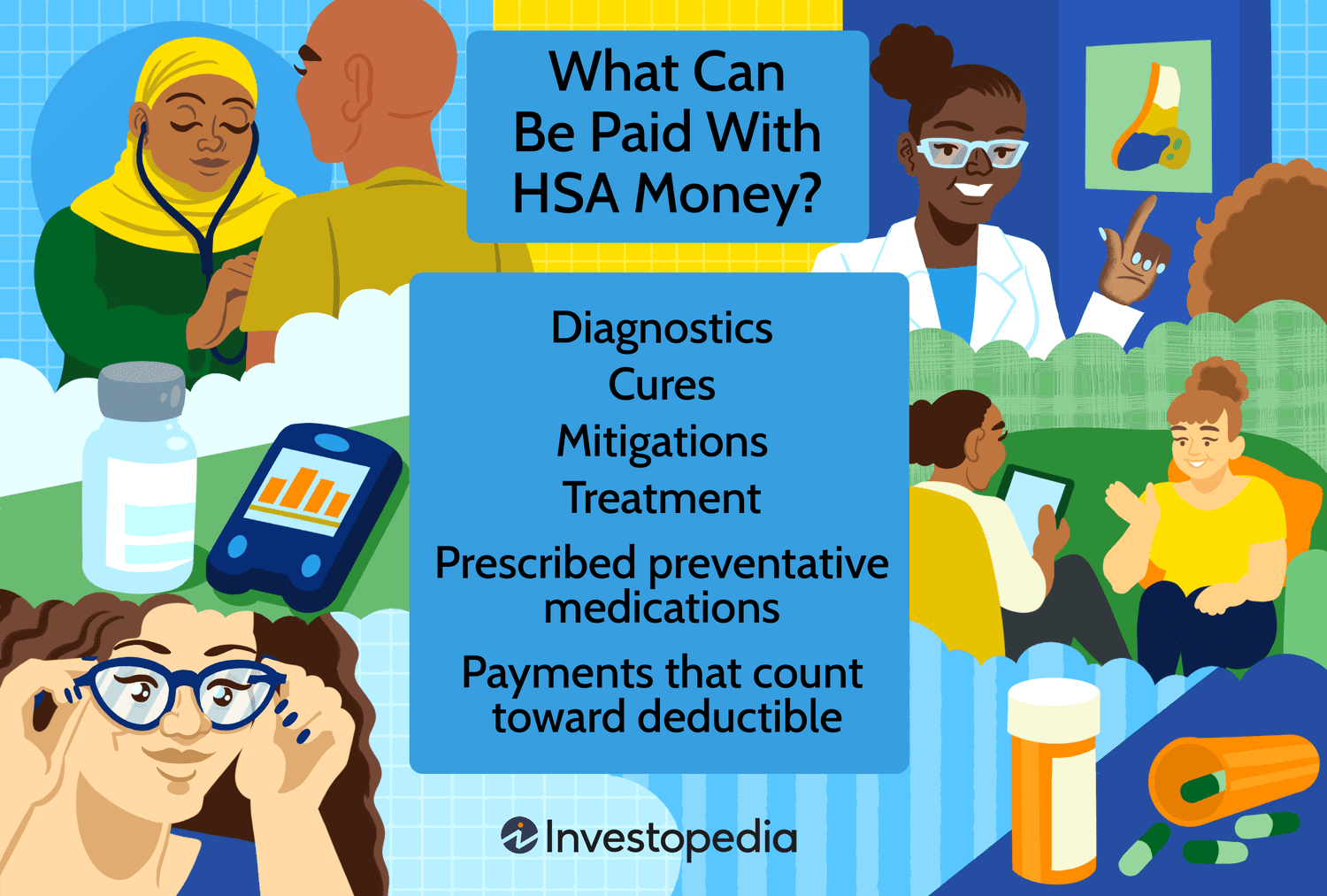

Qualified Expenses

HSA funds can be used for a wide range of eligible expenses, including:

-

Primary and specialist doctor visits

-

Prescription medications

-

Mental health services

-

Dental and vision care

-

Medical equipment and supplies

If you use HSA funds for non-medical expenses before age 65, you’ll pay income tax plus a 20% penalty. After age 65, you can use the funds for any purpose without penalty, though non-medical withdrawals will be taxed as income.

HSA vs. FSA: What’s the Difference?

| Feature | HSA | FSA |

|---|---|---|

| Ownership | Individual | Employer |

| Rollover | Yes (no expiration) | Usually no (limited rollover) |

| Portability | Yes | No |

| Investment option | Yes (if balance threshold met) | No |

| Eligibility | Must have HDHP | Available with any health plan |

Conclusion

Health Savings Accounts offer a smart way to save for current and future medical expenses while enjoying major tax advantages. If you’re enrolled in a high-deductible health plan, an HSA can provide financial flexibility and security for your health care needs—now and in the years ahead.